|

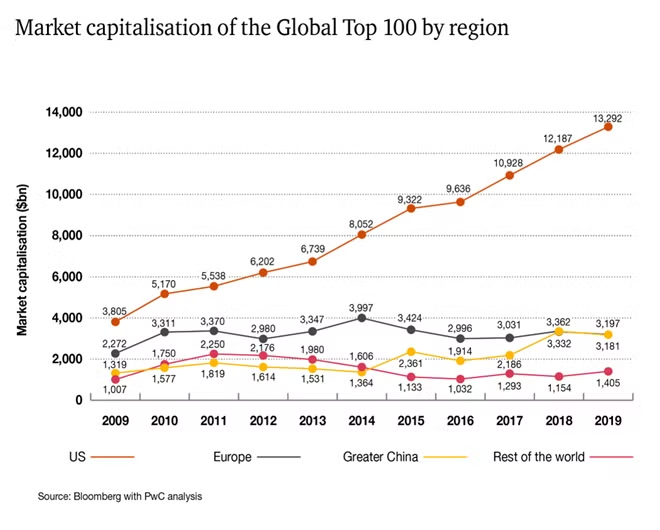

The rise is more subdued than the 15% increase reported in 2018, reflecting more challenging market conditions. Growth in market capitalization in the past year has been primarily driven by US companies, on the back of a robust economic environment.

Both Greater China (-4%) and Europe (-5%) registered a decrease in market capitalization, reversing last year’s gains. The technology sector continues to dominate, although the healthcare, consumer services and telecommunications sectors performed most strongly over the past year.

For the fifth year running, the US accounts for more than half (54) of the Global Top 100 by number of companies with growth of 9%, outpacing the overall.

US companies represent 63% of the total market capitalization, up from 61% last year. Greater China is the second largest component of the Global Top 100 by market capitalization, despite a 4% decline in the past 12 months following trade uncertainties and their impact on local market sentiment. This contrasts with the 57% increase in 2018, when three new companies entered the Global Top 100 and two rose to the top ten.

Geopolitical challenges including uncertainty on Brexit are likely to have impacted European based companies in the ranking in the past year. Three European based companies have left the Global Top 100 and overall European based companies in the ranking lost 5% in market capitalization.

The technology sector continues to be the largest component of market capitalization within the Global Top 100, ahead of the financial sector, with healthcare in third place. Growth in the healthcare, consumer services and telecommunications sectors of 15% outpaced technology’s growth (6%), which experienced volatility in late 2018.

Financials was the weakest performing sector with a 3% decline in market capitalization. The global top ten continues to be dominated by the technology and e-commerce companies – Microsoft, Apple, Amazon, Alphabet – followed by Facebook in sixth position and Alibaba and Tencent as numbers seven and eight, respectively.

Microsoft was the strongest performer in terms of absolute increase in market capitalization, gaining $202bn or 29% in value compared to 2018, which propelled it into the top spot. It’s followed by Apple, Amazon and Alphabet. This breakaway group is 40% ahead of the fifth ranked company, Berkshire Hathaway, which has a market capitalization of $494bn.

In the private company domain, the value of the top 100 unicorns grew by 6% to $815bn at 31 March 2019, consistent with their public company counterparts. Nearly half (48%) of the top 100 unicorns were from the US, also in line with what we see in the Global Top 100. Notably, Greater China contributes approximately 30% of unicorns in both number and value terms, which is a much higher proportion than for the Global Top 100.

As a significant source of future IPOs or acquisitions by other companies, this suggests that we can anticipate more entries from Greater China into the Global Top 100 in due course.